It turns out this interpretation, which has driven all Troika (ECB, IMF, and EU) and German/French policy input is badly flawed. It is correct for Greece. It is incorrect for the other four. Take a look at these charts, looking at three variables in three different charts: Net Government Lending (i.e., Deficits), total government debt as a percent of GDP, and the current account balance:

You can see that Spain and Ireland had lower debt levels than Germany; Portugal was essentially the same as Germany; and only Italy was significantly higher, starting in 1999 when the Euro began, at 110% and coming down in 2007 (just before the Crash) to just over 100%.

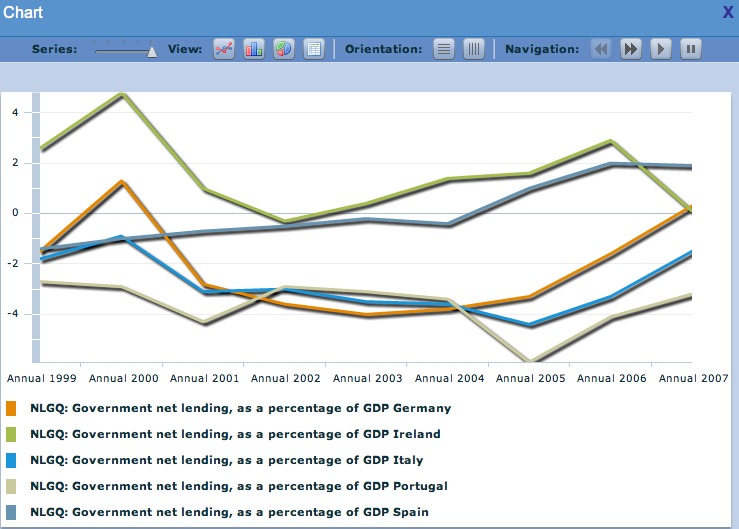

Now for Government Deficits:

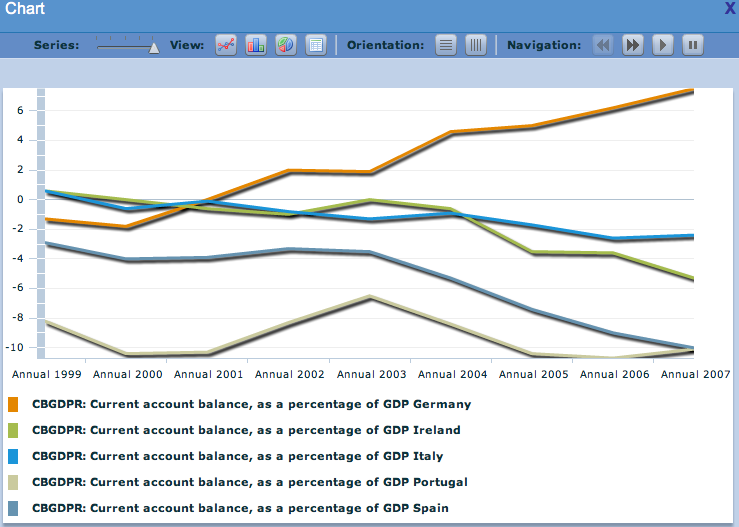

Ireland and Spain were doing better than Germany; Portugal and Italy, about the same. In Current Accounts, some differences do start to show up:

Germany was export positive; the others were net importers, with much of their imports coming from Germany. Was this profligate? I don't think so, although we will see in a minute how the bottom fell out after the 2008 Crash. Instituting the Euro eliminated exchange rate risk within the Eurozone. As a result, a lot of German and French money flowed to the periphery, where returns were judged to be higher. When the markets froze in 2008, this "hot" money dried up and countries had to fund these balances with Government debt, precipitating our current crisis. Here's an extended chart, showing what happened when the crisis hit in 2008:

Deficits blew up, wildly so for Ireland (whose Government assumed all the liabilities of their busted banks); seriously for Spain and Portugal; mildly for Italy and Germany.

Again, I have left Greece out of this picture. Their deficits were too large; their debt was speeding upwards; and their current account balances were deeply in the hole. In addition, with the help of Goldman and some fancy CDS trades/swaps, they masked a good portion of their debt, in order to gain admission to the Eurozone. Bad actors.

But Italy, Ireland, Portugal and Spain are being tarred with the same brush, which is unfair. They each ran pretty tight ships in terms of deficits and Government borrowing (Italy was high, but it had been in the 120% range through all of the 1990s', before Maastricht, and after 1998, they were bringing it down). Portugal, Ireland, Spain, and Italy generally ran current account deficits, but these were offset by new capital investments from other, mostly North European sources. In other words, smooth sailing and reasonably well run ships.

When the 2008 Crisis hit, and the markets froze, and the hot capital money dried up, the big troubles began. It was then that the fundamental flaws in the Eurozone became apparent: when a country with its own currency gets in trouble, and they cannot finance their import surplus, the currency drops, prices adjust, imports go down and exports go up, eventually bringing the system back to balance. In the Eurozone, once the capital inflows stopped after 2008, the trouble began, and there was no way left to adjust.

Enter austerity plans from the Troika, speaking from the morality tale platform, essentially commanding these "wayward countries" to cut the crap and get in line. The apparently preferred, mostly German solution is more fiscal integration, possibly Eurobonds, but definitely a central authority with the power to put in place serious penalties when a country's fiscal position gets out of line.

What is needed instead (I believe) is not beating your export customers over the heads (i.e., Germany vs. the "profligate South"), rather it's an ongoing way to provide "vendor financing" on a long term basis, or a continuing program of investing in the peripheral, less competitive economy.

Continuing on the current course must, I believe, lead to breakdown of the Eurozone. The fiscal integration path, with only sticks and no carrots, won't endure over time.

We should remember that most morality tales don't always turn out with happy endings for all. I am convinced that if the Troika and Germany could take off their morality lenses, we would have a much better chance of finding a good and fair resolution. I am afraid, though, that this will not happen, and that we are witnessing a slow-rolling train wreck.

No comments:

Post a Comment